PREVIOUS

✖

Economic Survey 2025/2026 - Part 01

February 13 , 2025

4 hrs 0 min

58

0

Economic Survey 2025/2026 - Part 01

(இதன் தமிழ் வடிவத்திற்கு இங்கே சொடுக்கவும்)

Introduction

Preparation and Presentation

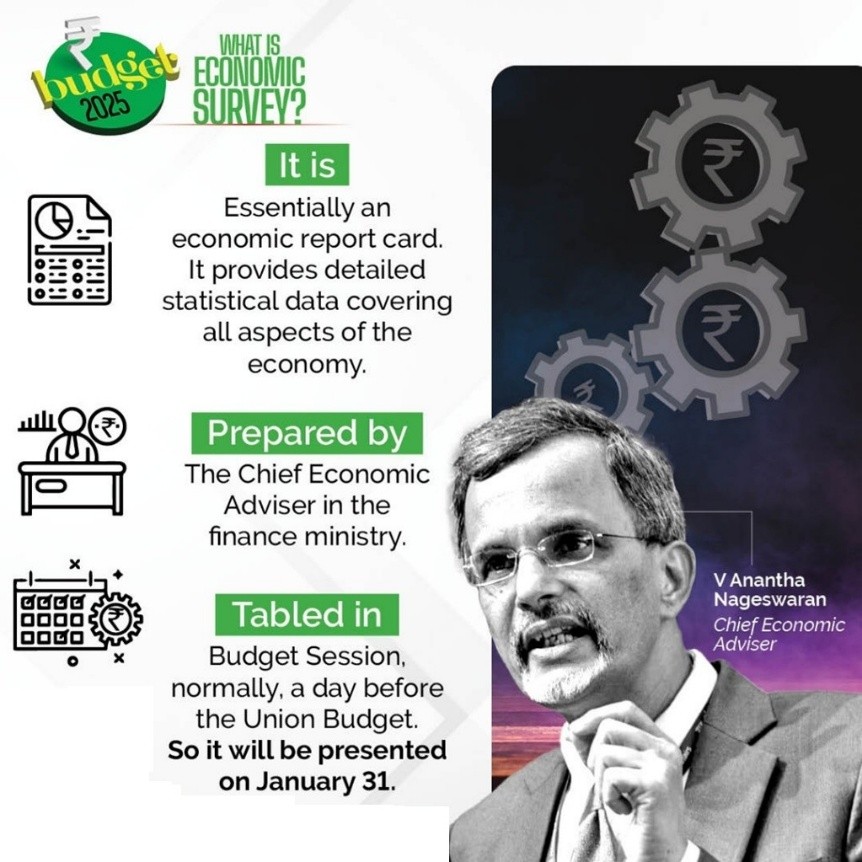

· The Economic Survey is prepared by the Chief Economic Adviser (CEA), V Anantha Nageswaran, and his team.

· It was presented in the Lok Sabha by Nirmala Sitharaman, the Union Minister of Finance and Corporate Affairs.

Focus Areas

· Focuses on India’s economic outlook and growth projections.

· Highlights structural reforms and medium-term growth strategies.

Global and Domestic Context

· It discusses global economic shifts and their potential impact on India.

· Outlines India’s developmental priorities and key policy focus areas.

Growth Projections

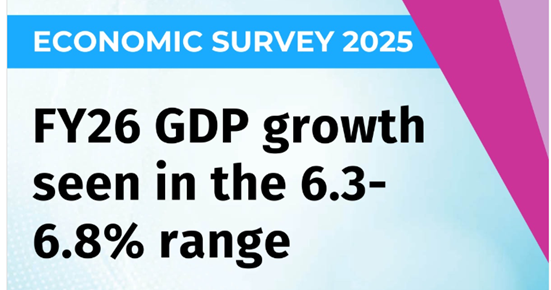

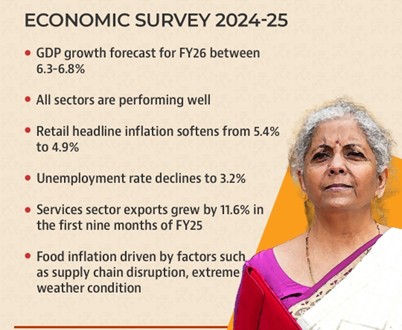

· India’s economy is expected to grow between 6.3% and 6.8% in FY26.

Real GDP and GVA Growth

· Real GDP Growth: Estimated at 6.4% for FY25 (First Advance Estimates).

Structural Reforms and Global Competitiveness

· Grassroots-Level Structural Reforms: Focus on deregulation and boosting growth potential and global competitiveness.

· Geo-Economic Fragmentation: Globalization is being replaced by geo-economic fragmentation, causing economic realignments.

· Ease of Doing Business 2.0 & SME Development: Emphasis on reforms to foster entrepreneurship and grow India’s Mittelstand (MSME sector).

Infrastructure and Private Sector Participation

· Private Sector Participation: Crucial for meeting the growing infrastructure requirements.

· Capital Expenditure (CapEx): Continuous improvement from FY21 to FY24, with an 8.2% YoY growth post the general elections.

· Growth in Infrastructure Capital Expenditure: 38.8% growth from FY20 to FY24 in key infrastructure sectors.

Inflation and Credit Growth

· Inflation Projections: RBI and IMF project India’s consumer price inflation to align with the 4% target by FY26.

· Retail Inflation: Reduced from 5.4% in FY24 to 4.9% during April–December 2024.

· Bank Credit Growth: Steady growth with credit growth aligning with deposit growth.

· Non-Performing Assets (NPAs): Gross NPAs of scheduled commercial banks at a 12-year low of 2.6%.

Financial and Investment Milestones

· Insolvency and Bankruptcy Code (IBC): ₹3.6 lakh crore realized through the resolution of 1,068 plans by September 2024.

· Equity and Debt Mobilization: ₹11.1 lakh crore mobilized by December 2024, marking a 5% increase from the previous year.

· Stock Market Capitalization: BSE stock market capitalization to GDP ratio at 136%, higher than China (65%) and Brazil (37%).

Trade and Export Performance

· Overall Export Growth: Overall exports (merchandise and services) grew by 6% YoY in the first nine months of FY25.

· Services exports increased by 11.6% during the same period.

· Services Export Growth: Services export growth surged to 12.8% during April–November FY25, up from 5.7% in FY24.

· Global Ranking in Telecommunications & IT Services: India is the 2nd largest exporter globally in 'Telecommunications, Computer, and Information Services' (UNCTAD).

Foreign Exchange Reserves and Debt

· Foreign Exchange Reserves: Forex reserves reached USD 640.3 billion by December 2024, covering 10.9 months of imports and approximately 90% of external debt.

Innovations and Space Vision

· Space Vision 2047: Key missions include Gaganyaan and Chandrayaan-4, focusing on lunar sample return.

· Smartphone Manufacturing: 99% of smartphones are now manufactured domestically, drastically reducing imports.

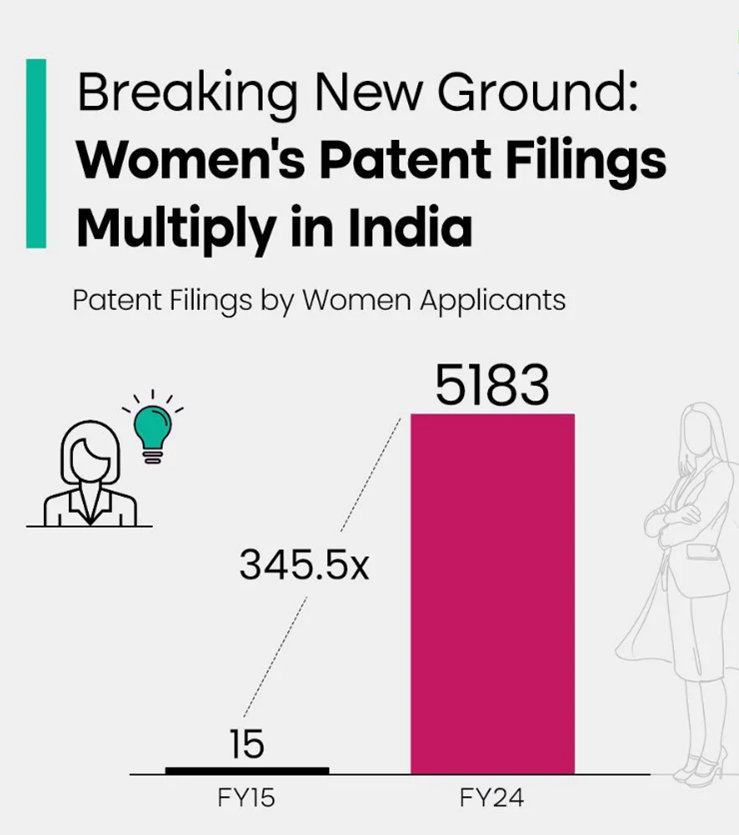

· Intellectual Property: India ranks 6th globally for patent filings according to WIPO’s 2022 report.

Support for MSMEs and Self-Reliance

· Self-Reliant India Fund: ₹50,000 crore allocated to provide equity funding to MSMEs.

Agriculture and Allied Sectors

· Contribution of Agriculture: Agriculture and allied activities contributed approximately 16% to India’s GDP for FY24 at current prices.

· Kharif Foodgrain Production: Expected to reach 1,647.05 LMT, an increase of 89.37 LMT from the previous year.

· Growth in Fisheries and Livestock: Fisheries sector has a CAGR of 8.7%, while livestock shows a CAGR of 5.8%.

Renewable Energy and Sustainability

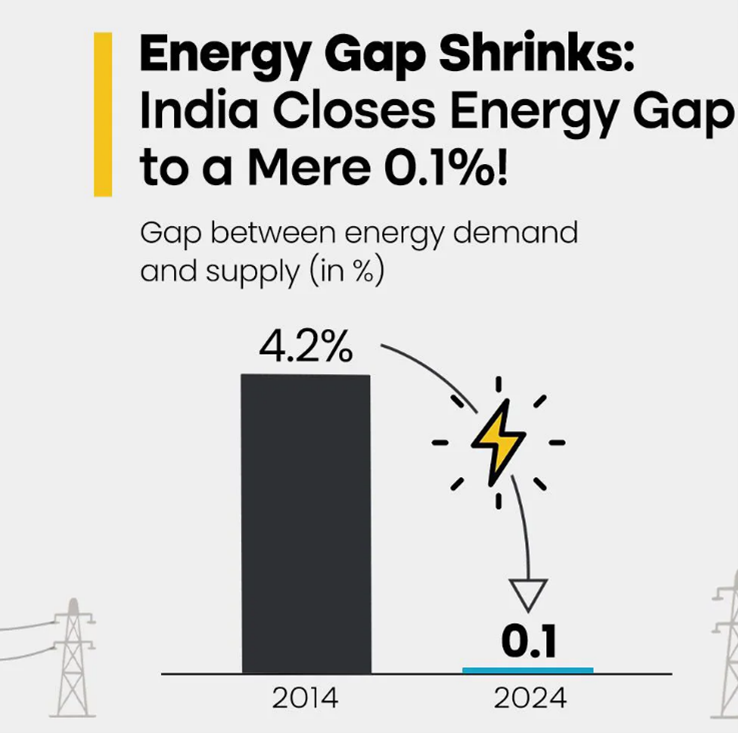

· Electricity Generation from Non-Fossil Fuels: Non-fossil fuel electricity generation accounts for 46.8% of total capacity.

· Carbon Sink Creation: Created an additional carbon sink of 2.29 billion tonnes of CO2 equivalent between 2005 and 2023.

· Life Measures for Global Consumers: Life measures could save around USD 440 billion globally by 2030.

Social Services and Employment

· Government Health Expenditure: Health expenditure by the government increased from 29% to 48%, while out-of-pocket health expenses by people decreased from 62.6% to 39.4%.

· Social Services Expenditure Growth: Social services expenditure grew at an annual rate of 15% from FY21 to FY25.

· Unemployment Rate: Declined to 3.2% in 2023-24, down from 6.0% in 2017-18.

Digital Economy and Job Creation

· Growing Digital Economy and Renewable Energy: These sectors are key for job creation and are integral to realizing Viksit Bharat's vision.

· PM-Internship Scheme: The scheme has become a transformative catalyst for employment generation.

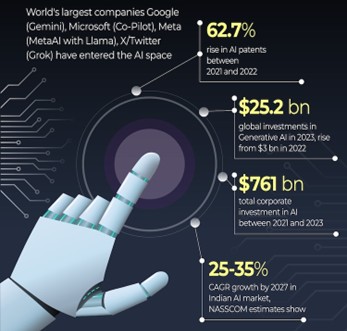

AI Adoption and Policy Measures

· Barriers to Large-Scale AI Adoption: Barriers persist, providing policymakers an opportunity to address challenges.

· Collaborative Efforts for AI-Driven Transformation: The Collaboration between government, private sector, and academia is crucial to minimize adverse societal effects of AI-driven transformation.

State of the Economy: Getting Back into the Fast Lane

· Real GDP Growth: Estimated at 6.4% for FY25, aligning with the decadal average.

· Real GVA growth projected at 6.4% for FY25.

· Global Economic Context: The global economy grew by 3.3% in 2023.

· This growth was slightly ahead of the IMF's forecast of 3.2% for 2023.

· The IMF forecasts an average growth rate of 3.2% for the next five years (2024-2028).

· Future Growth Projections: Real GDP growth for FY26 expected between 6.3% and 6.8%, factoring in both upsides and downsides.

· Structural Reforms: Focus on grassroots-level reforms and deregulation to strengthen medium-term growth and global competitiveness.

· Global Challenges: Geopolitical tensions, ongoing conflicts, and global trade policy risks present challenges to the global economic outlook.

Exports and Global Competitiveness:

· India holds the 7th largest share in global services exports.

· Non-petroleum and non-gems & jewellery exports grew by 9.1% during April–December 2024, showcasing resilience despite global volatility.

Monetary and Financial Sector Developments:

Bank Credit and Performance:

· Bank credit has grown steadily, aligning with deposit growth.

· SCB profitability improved, with a decline in GNPAs and an increase in the CRAR.

· Credit Growth: Credit growth has outpaced nominal GDP growth for two consecutive years, with the credit-GDP gap narrowing to -0.3% in Q1 FY25 from -10.3% in Q1 FY23.

Asset Quality:

· GNPAs of SCBs fell to a 12-year low of 2.6% of gross loans and advances by September 2024.

· Insolvency and Bankruptcy Code (IBC): ₹3.6 lakh crore realized through 1,068 IBC resolutions by September 2024, representing 161% of liquidation value and 86.1% of the fair value of assets involved.

Stock Market Performance:

· Indian stock markets outperformed emerging markets despite election-related volatility.

· Primary market resource mobilization (equity and debt) reached ₹11.1 lakh crore between April–December 2024, marking a 5% increase from FY24.

Insurance and Pension Growth:

· Insurance premiums grew by 7.7% in FY24, reaching ₹11.2 lakh crore.

· Pension sector grew significantly, with the total number of pension subscribers rising by 16% YoY as of September 2024.

External Sector: Getting FDI Right

External Sector Resilience:

· India’s external sector remains resilient despite global uncertainties.

Global Export Ranking:

· India holds 10.2% of the global export market in ‘Telecommunications, Computer, & Information Services,’ ranking as the second-largest exporter (UNCTAD).

Current Account Deficit (CAD):

· CAD stood at 1.2% of GDP in Q2 FY25, supported by rising net services receipts and increased private transfer receipts.

Foreign Direct Investment (FDI):

· FDI inflows revived, increasing from USD 47.2 billion in the first eight months of FY24 to USD 55.6 billion in FY25, marking a 17.9% YoY increase.

External Debt:

· External debt remained stable, with the external debt-to-GDP ratio standing at 19.4% by September 2024.

Prices and Inflation: Understanding the Dynamics

Global Inflation Trends:

· Global inflation moderated to 5.7% in 2024, down from 8,7% in 2022 (IMF).

India’s Inflation:

· Retail inflation in India reduced from 5.4% in FY24 to 4.9% in FY25 (April–December 2024).

Inflation Targeting:

· RBI and IMF forecast India’s consumer price inflation to gradually align with the target of around 4% by FY26.

Climate-Resilient Agriculture:

· Development of climate-resilient crop varieties and improved farming practices are key to mitigating extreme weather effects and ensuring long-term price stability.

-------------------------------------

Leave a Reply

Your Comment is awaiting moderation.