PREVIOUS

✖

Right to tax mineral-rich lands

July 30 , 2024

9 hrs 0 min

18

0

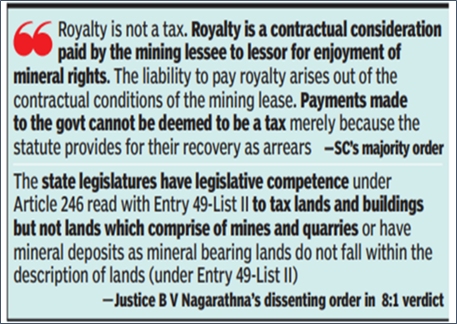

- The Supreme Court held that, the power of State Legislatures to tax mining lands and quarries is not limited by the Parliament’s Mines and Minerals (Development and Regulation) Act of 1957.

- It frees states from the restrictions of the Centre and is in tune with the federalist principles of governance.

- State Legislatures derive their power to tax mines and quarries under Article 246 read with Entry 49 (tax on lands and buildings) in the State List of the Seventh Schedule of the Constitution.

- Mineral bearing lands fall within the description of ‘lands’ in Entry 49.

- But centre had argued that Entry 50 in the State List had allowed the Parliament to impose “any limitations” on taxes on mineral rights through laws relating to mineral development.

- The verdict further clarified that royalty paid by those who lease mines to the government is not tax.

- The case has its genesis in a dispute between India Cement Ltd and the Tamil Nadu government of 1989.

Leave a Reply

Your Comment is awaiting moderation.